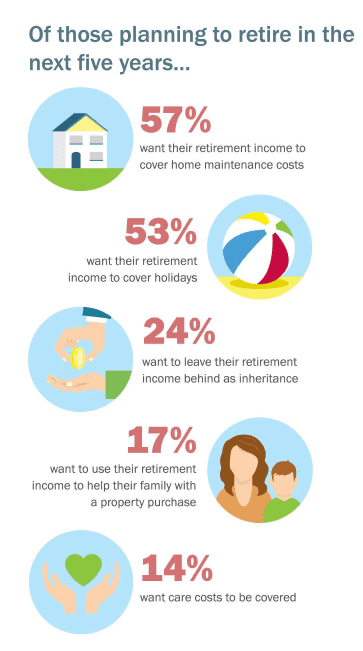

Retirement can make up a big chunk of your life. And we have varying aspirations of what we want from retirement, as the infographic shows. But although many of us know what we want, surprisingly few of us take professional advice to make sure we have a fighting chance of getting the retirement we desire.

People who may need advice don’t seek it: Around 40% of people who took out an investment didn’t take advice, and this rises to 78% of people who took out a personal pension*.

Is it worth having a Financial Advisor?

‘The Value of Financial Advice’ report from the International Longevity Centre think-tank, published in July 2017 makes interesting reading.

- The report found that advised consumers were, on average, £40,000 better off than their non-advised counterparts.

- Over eight in ten (81%) of those who took advice feel confident that they’ve made the right choice about what to do with their money.

- 75% say financial advice helped them get more for their money.

- 19% who didn’t take financial advice say even though they don’t regret it now, they worry they might in the future.

- The self-employed are 6 percentage points more likely to receive expert financial advice than “employees”. And they are a further 6 percentage points more likely to act on it.

Retirement planning is particularly challenging today because of the increasing responsibility being placed on us all. In times gone by, you might typically have retirement income to complement your state pension. This might have happened through a final salary pension scheme or defined benefit (DB) plan.

But because we are living longer, DB schemes are now deemed unsustainable and closed to new entrants, and have been largely replaced with defined contribution (DC) schemes. Unlike DB schemes, when saving into a DC scheme, it is up to us to choose how much we want to contribute. So nowadays, we need to be able to calculate how much we need to save to be able to retire when we want to and have a reasonable or good lifestyle. Unsurprisingly, most of us don’t do this.

We’re in the driving seat, but no-one taught us how to drive

Guess what? Most of us don’t know how much money we will need for our retirements. Why? Well, we weren’t taught how to calculate it because our parents didn’t need to. They might have been on DB schemes where the pot was automatically converted to an income which paid out every month and was calculated on their final salaries or average earnings.

Not only are most of us not experts on annuity tables, neither are we adept at modelling asset growth, inflation and planning long term outgoings. As a result, many of us are simply “going blind” and guessing how much to put into our pension each month with no real knowledge of whether it will be enough.

It’s human nature

Guess what? Contribution rates are not nearly high enough to guarantee adequate income in retirement. Why? Because our income is limited and it’s human nature to make a conservative estimate given the absence of knowledge, as to how much to put into our pension funds.

In addition, the recent introduction of the “pension freedoms” allow people to choose whichever retirement route they see fit, including cashing in the entire DC pot, entering an income drawdown arrangement or buying an annuity. It is critical in this complex environment to make sure that we plan to have enough income available for the remaining years.

So, although many of us have some general ideas of what we might want from retirement, my experience is that not many of us have costed it out and worked out how much money is enough to fund it.

Start planning now

Historically, not everyone has viewed financial advice as a necessary commodity. But when you factor in how much we are now all responsible for our own retirement destinies, the landscape is changing dramatically. The report is a welcome indication of that and also an endorsement, I think, of the benefits of taking advice.

My advice to you? Start planning now.

Yours

John Davies

| Book a free consultation with John or Richard to find out how to make the best of your retirement.

Click here to arrange a call or meeting. |

References

- *The Value of Financial Advice’ report (July 2017) International Longevity Centre

- Preparing for retirement LV=