The amount of Income Tax paid to HMRC has doubled since the turn of the millennium. With tax bands now frozen until 2026, more workers are likely to find themselves in the higher- or additional-rate tax band. It means it’s more important than ever to make use of allowances to make your money go further.

In the 1999/2000 tax year, £93 billion was paid in Income Tax, according to a Financial Times report. The most recent figures for 2018/19 show that that figure more than doubled to £187 billion. For the current 2021/22 tax year, HMRC predicts that £199 billion will be paid in Income Tax.

The rise is partly linked to the number of workers paying Income Tax. In 1999/2000, there were around 27.2 million taxpayers, compared to 31.6 million in 2018/19. But the tax brackets freezing is likely to have a huge impact over the next few years.

Why does freezing tax brackets matter?

In the 2021 Budget, chancellor Rishi Sunak had to address the hole left in public finances by the pandemic. Rather than increase Income Tax, he froze Income Tax bands. This has been dubbed a “stealth tax”.

Usually, Income Tax thresholds would increase each tax year in line with inflation. This preserves workers’ spending power as the cost of living rises because, as wages increase, the amount you continue to pay in Income Tax remains broadly in line with this. However, tax bands are now frozen up to the 2025/26 tax year.

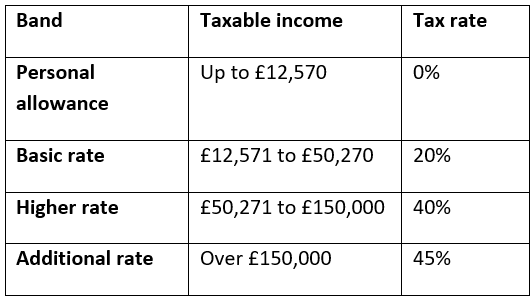

The Income Tax thresholds in England are expected to remain:

This freeze means thousands more people will find themselves in a higher tax bracket, even though they’re no better off when you factor in inflation. HMRC estimates that there will be an extra 440,000 additional-rate taxpayers in 2021/22, an increase of 10.3% when compared to 2018/19.

With more of your money potentially going to HMRC through Income Tax, it’s more important than ever that you make use of tax allowances to make your money go further.

Here are two allowances to consider in your financial plan.

1. ISA allowance

If you’re a higher- or additional-rate taxpayer, you may have to pay tax on your savings. The personal savings allowance (PSA) lets basic-rate taxpayers earn up to £1,000 in interest without paying tax on it. However, this falls to £500 for higher-rate taxpayers, and additional-rate taxpayers do not benefit from the PSA.

So, finding a home for your savings that minimises tax is important. An ISA offers a way to save without incurring additional tax. For the 2021/22 tax year, you can place up to £20,000 into ISAs.

ISAs also offer a tax-efficient way to invest. Opting for a Stocks and Shares ISA, rather than a Cash ISA, means your savings are invested and returns aren’t taxed. If you have long-term goals, a Stocks and Shares ISA can make financial sense. You need to consider the investment risks you’ll be exposed to but, as a high earner, a Stocks and Shares ISA can help you make the most of your money.

2. Pension Annual Allowance

As a higher- or additional-rate taxpayer, you can benefit more when contributing to your pension.

Tax relief is paid at the highest rate of Income Tax you pay. So, as a higher-rate taxpayer you can receive 40%, or 45% if you’re an additional-rate taxpayer. It can give your retirement savings an instant boost. To add £100 to your pension, you’d need to pay just £60 or £55, respectively.

Usually, your pension provider will claim 20% tax relief for you. To receive the extra relief due, you’ll need to complete a self-assessment tax return.

However, you can’t simply put as much as you can in your pension and benefit from tax relief on all contributions. The Annual Allowance limits how much you can claim each tax year. Usually, this is £40,000 or 100% of your annual earnings, whichever is lower. However, if your annual income is more than £200,000 you may be affected by the tapered Annual Allowance, which could reduce your allowance by up to £36,000. If you’re not sure what your Annual Allowance is, please contact us.

If you’re increasing your pension contributions, you need to be mindful of the Lifetime Allowance. This is the total amount you can hold in your pension in your lifetime without incurring additional tax charges.

For the 2021/22 tax year, the Lifetime Allowance is £1,073,100. This allowance is also frozen until 2026. That figure may seem high, but this threshold doesn’t just consider your contributions; it also considers the total value of your pension. This includes employer contributions, tax relief, and investment returns, so it can be easier to exceed this threshold over your working life than you might think.

If you’d like to talk about how to reduce your tax liability and get the most out of your money, please give us a call. We’re here to help you put a tailored plan in place to suit your goals.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.

Please note that the information provided in this article was correct at the time of publishing.